Why Selling Before Donating Is a Costly Tax Mistake (Stock, Crypto, Real Estate Examples)

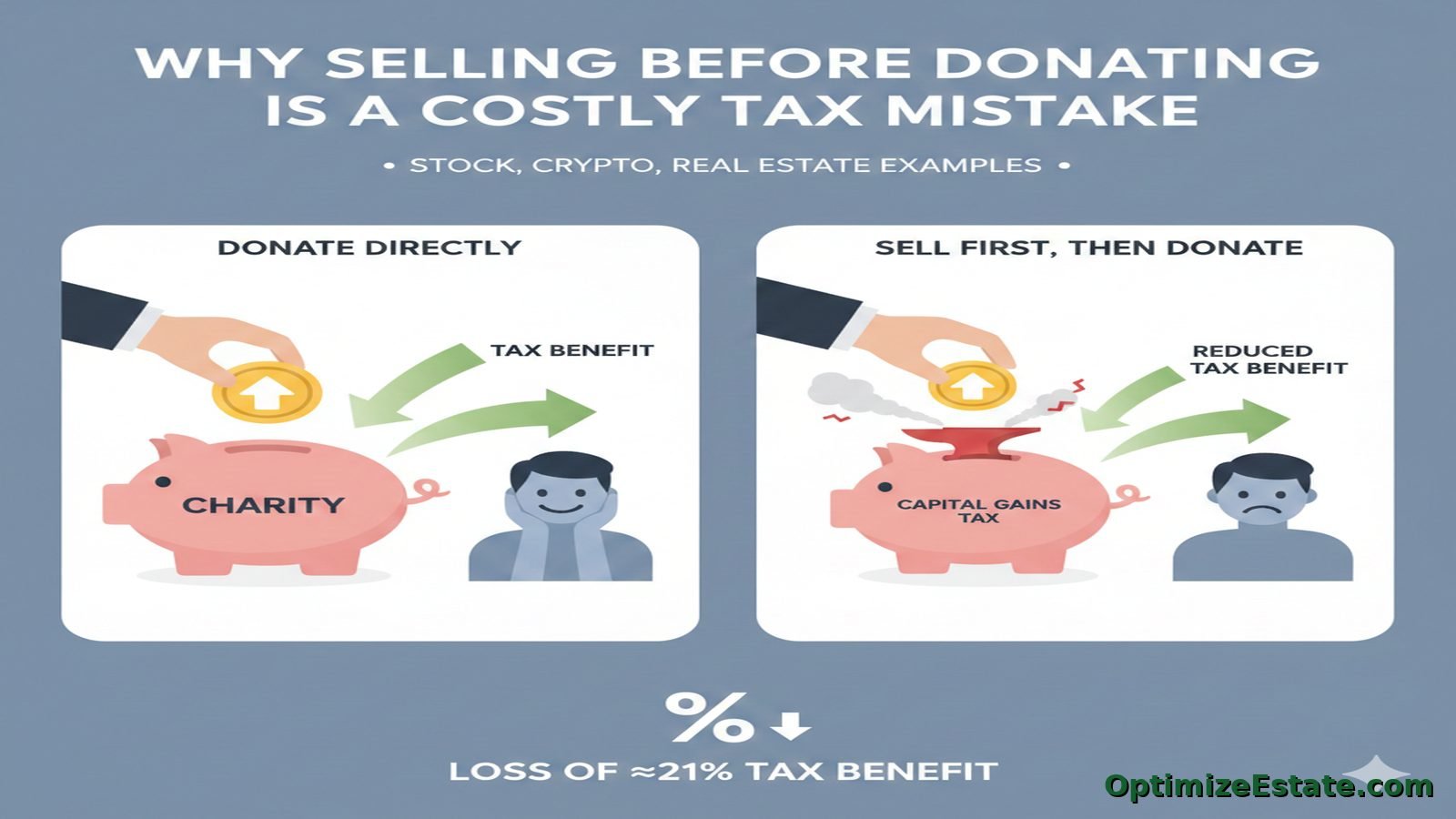

Most people understand that donating appreciated assets can reduce taxes. What far fewer people realize is how much money is lost simply by selling first, even when the donation amount feels almost the same.

The difference is not subtle. It comes down to whether capital gains tax is triggered before the donation happens.

The baseline asset

Assume you own an appreciated asset with:

• Fair market value: $100,000

• Original cost basis: $50,000

• Unrealized long-term capital gain: $50,000

You are a high-income earner subject to top federal income tax, Net Investment Income Tax, and state income tax.

For long-term capital gains, a combined rate of approximately 30% typically reflects:

• 20% federal long-term capital gains

• 3.8% Net Investment Income Tax

• 6–10% state tax

This combined rate commonly applies to high earners in states such as California, New York, New Jersey, Massachusetts, and Oregon.

Donating appreciated assets directly

You donate the $100,000 appreciated asset directly to a Donor-Advised Fund.

What happens:

• Capital gains tax triggered: $0

• Amount deducted: $100,000 (fair market value)

• Ordinary income tax avoided: approximately $59,000

Effective outcome:

• Asset value donated: $100,000

• Tax saved: about $59,000

• Effective benefit rate: roughly 59%

This result comes from combining two effects:

1) Capital gains are never realized

2) The full fair-market-value deduction offsets high marginal income

This framework is explained in detail in the article titled “How High W-2 Earners Can Cut Taxes 50%+ by Donating Appreciated Assets (2026 Update).”

Selling first, then donating

Now assume the same asset, same value, and same intent, but the asset is sold first.

Step one is the sale:

• Sale price: $100,000

• Cost basis: $50,000

• Long-term capital gain: $50,000

Capital gains tax owed:

• $50,000 × 30% = $15,000

This $15,000 is a real cash outflow. It is paid from the asset proceeds and cannot be recovered or offset later.

Cash remaining after tax:

• $100,000 − $15,000 = $85,000

Step two is the donation:

• Donation amount: $85,000

• Deduction allowed: $85,000

Ordinary income tax avoided:

• $85,000 × approximately 45% = about $38,250

The key point is that the capital gains tax is already gone. The only tax benefit created is the deduction on the smaller donation.

Side-by-side comparison

| Donate Appreciated Asset Directly | Sell First, Then Donate | |

|---|---|---|

| Asset fair market value | $100,000 | $100,000 |

| Cost basis | $50,000 | $50,000 |

| Capital gains realized | $0 | $50,000 |

| Capital gains tax paid (≈30%) | $0 | $15,000 |

| Amount available to donate | $100,000 | $85,000 |

| Charitable deduction allowed | $100,000 | $85,000 |

| Ordinary income tax avoided (≈45%) | $59,000 | $38,250 |

| Total effective tax benefit | $59,000 (≈59%) | $38,250 (≈38%) |

| Tax benefit lost by selling first | $20,750 | |

Nothing about the asset changed.

Nothing about the generosity changed.

Only the order of operations changed.

Why this applies beyond stocks

Although stocks make the math easy to illustrate, the same logic applies to many asset types, often with even larger consequences.

This includes:

• Public stocks and ESPP shares

• Crypto assets

• Real estate

• Art and collectibles

• Alternative investments and private assets

Assets with large embedded gains suffer the most damage when sold first. This is why many non-cash assets are among the most powerful to donate directly.”

When selling first may still make sense

There are limited situations where selling first can be reasonable:

• The asset has little or no appreciation

• The gain is short-term and minimal

• Liquidity timing is critical

• The asset is not eligible for direct donation

Outside of these cases, selling before donating is usually not a strategy. It is a structural tax mistake.

Advanced Guides & Deep Dives

- How High W-2 Earners Can Cut Taxes by 50%+ by Donating Appreciated Assets (2026) Best if you want the core strategy and the math: why donating appreciated assets can stack ordinary-income savings plus avoided capital gains for a 50%+ effective benefit.

- Three Powerful Steps for a Donor-Advised Fund: Donate High, Invest Low, Grant Later Best if you want a simple operating framework: contribute in a high-income year, invest inside the DAF, and grant over time without rushing charity choices.

- DAF vs CRT Deduction Limits Under the Big Beautiful Bill Best for high-income technical planning: Compare how the 0.5% AGI floor and 35% benefit cap uniquely impact DAFs versus CRTs so you can choose the vehicle that maximizes your 2026 deduction.

- DAF vs CRT: Donor-Advised Fund vs Charitable Remainder Trust Best if you’re planning for 2026+: understand how deduction limits and thresholds may change outcomes for high-income donors using DAFs or CRTs.

Frequently Asked Questions

Does this strategy only apply to assets held long term?

Yes.

The primary tax benefit of donating appreciated assets comes from avoiding long-term capital gains tax, which generally requires the asset to be held for more than one year. Assets held for one year or less are typically treated as short-term and do not receive the same tax advantage when donated.

Can donated assets be invested while they sit inside a DAF or CRT?

It depends entirely on the administrator.

Some sponsors allow broad investment flexibility, while others restrict assets to a limited menu or require rapid liquidation. These operational differences can materially affect outcomes, especially when timing, volatility, or liquidity matter.

Do all DAF and CRT administrators accept the same types of assets?

No.

Acceptance policies vary widely. Some administrators only support publicly traded securities, while others can handle private investments, real estate interests, or digital assets. Choosing an administrator that aligns with the assets you plan to donate is critical to executing the strategy correctly.